Introduction to Economics

The roots of education are bitter, but the fruit is sweet.

—attributed to Aristotle by Diogenes Laërtius

Overview

Discuss the importance of studying economics

Explain the relationship between production and division of labor

Evaluate the significance of scarcity

Core Concepts

- Economics

the study of decision making in the face of scarcity

- Decisions

individual, family, business or societal.

- Scarcity

the desire for goods, services and resources exceeds availability.

- Resources

land, labor (time), capital (tools, equipment, buildings), human capital

limited in supply

used to produce goods and services

Introduction to FRED

- Economic data

describe and measure the economics concepts

- FRED

Federal Reserve Economic Data

online display as tables or charts

easily downloadable

Video: What Is FRED?

Coping with Scarcity: Two Options

each produces everything s/he consumes

“jack of all trades, master of none”

each produces something and then trades for consumption

division and specialization of labor

described by Adam Smith in The Wealth of Nations (1776)

pin manufacturing example (18 distinct tasks)

Adam Smith, 1723–1790

Adam Smith

Source: Stefan Schäfer

Productivity and the Divison of Labor

Benefits from:

current competency: specialization according to skills, talents, and interests

acquired competency: specialization -> quicker learning

economies of scale: larger organization size -> lower costs per unit

Costs from:

resulting need to trade

Why Learn Econ?

understand the world

critically evaluate arguments - when is “common sense” actually nonsense?

promote good policy (e.g., when voting)

but, “good” depends on your objectives

Micro vs Macro

- Microeconomics

Individuals and particular markets (e.g., determinants of the price and quantity of a good). Emphasize on constrained choice.

- Macroeconomics

The economy as a whole (e.g., determinants of inflation and unemployment). Emphasis on emergent outcomes.

Microeconomic Questions: Some Examples

how do individuals make trade-offs among goods and services?

how do individuals make trade-offs between saving and consumption?

how do firms decide what to produce and how?

how does a market determine price and quantity?

how do taxes affect the decisions of individuals and firms?

Macroeconomic Questions: Some Examples

what is the overall level of production in a society?

how is the overall level of production changing over time in the short run?

how is the overall level of production changing over time in the long run?

what determines the overall level of production?

how can we compare the standard of living across countries?

what determines the social distribution on income and wealth?

how do monetary and fiscal policy affect the economy in the short run and long run?

Theories and Models

What Is a Theory?

more than just an idea or hunch,

a system of ideas that helps us organize our interpretations of a system.

an explanatory framework for a domain of possible experiences.

- physical sciences

reserve the term ‘theory’ for hypotheses that are widely accepted due to the weight of the accumulated evidence

- social sciences

use the term ‘theory’ just to mean an abstract model plus a hypothesis

What Is a Scientific Theory?

a scientific theory generates scientific hypotheses.

- scientific hypothesis

observations must be able to affect the credibility of the theory

experience (observations) can force revisions to beliefs (about the accuracy of the theory).

If we are committed to a theory regardless of the evidence, we are not doing science. A scientific theory is vulnerable to the evidence.

Systems and Models

- model

characterizes a real or imaginary system, known as the target system.

- system

an object or process with components, along with

the structure of their interrelations.

Model Development

- Model development

efforts to conceptualize, implement, or improve a model.

- ignores many real-world features

some are too costly to consider

some are judged to be irrelevant (to the model-development goals)

Model Development Process

Sometimes model development is purely verbal or graphical.

However, scientific model development often involves implementing the conceptual model as a mathematical model, computational model, or physical model.

Figure f:modelingProcess100 provides a stylized illustration of key steps in model development and analysis.

Stylized Representation of Modeling Process

Questions about Modeling

A “good” model helps us achieve the goals we had when creating it.

understand

predict

control

The usefulness of a model should be assessed in terms of its goals.

A pedagogical model may aid understanding without being useful for prediction.

A statistical model may help predict without adding much understanding.

A more realistic model need not be a more useful model.

Related question: what makes a map useful?

Can a map of Middle Earth be useful?

Two Camps: RAD vs. KISS

- Realism, Accuracy, and Detail (RAD):

realism is a virtue

create accurate and detailed representations of relationships

closer resemblance to nitty-gritty empirical investigations

- Keep it stylized and simple (KISS):

simplicity is a virtue

create highly stylized representations of relationships

closer resemblance to formal mathematical theory building

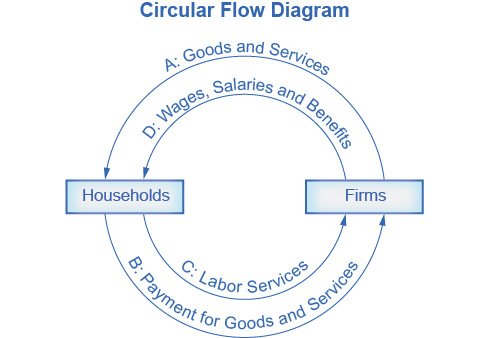

Simplified Circular Flow Diagram for the Macro Economy

Economic models often highlight interactions between different parts of the economy.

Circular Flow

Households and firms interacts in the markets for goods and services and in the labor market.

(Keeping it very simple!)

Video: Simplified Circular Flow Diagram

Video from the St Louis Fed (Economic Lowdown)

Epstein on Why We Model

[Epstein-2008-JASSS] offers 16 reasons other than prediction.

Explain (very distinct from predict)

plate tectonics and earthquakes; electrostatics and lightning; evolution and speciation

Guide data collection

Illuminate core dynamics

Suggest dynamical analogies

Discover new questions

Promote a scientific habit of mind

Bound (bracket) outcomes to plausible ranges

Illuminate core uncertainties.

Epstein on Why We Model (cont.)

Offer crisis options in near-real time

Demonstrate tradeoffs / suggest efficiencies

Challenge the robustness of prevailing theory through perturbations

Expose prevailing wisdom as incompatible with available data

Train practitioners

Discipline the policy dialogue

Educate the general public

Reveal the apparently simple (complex) to be complex (simple)

Economic Systems

Economic Systems: Traditional Economy

occupations stay in the family

most families farm traditional crops

produce what you consume

little economic progress or development

Economic Systems: Command Economy

government sets production goals and methods of production

government sets prices and wages

government may set low or zero prices on “necessities” (e.g., healthcare, education)

Examples: Pharonic Egypt; Medieval manor life

Examples: Cuba and North Korea have large command elements to their economies.

Economic Systems: Free-Market Economy

decentralized production decisions (private enterprise)

market supply and market demand determine prices and wages

even “necessities” (e.g., healthcare, education) are priced by the market

Economic Systems: Mixed Economy

most actual economies

combine market and command elements

entire spectrum from primarily free market to primarily command

likely subsidy of some “necessities” (e.g., basic healthcare, K12 education)

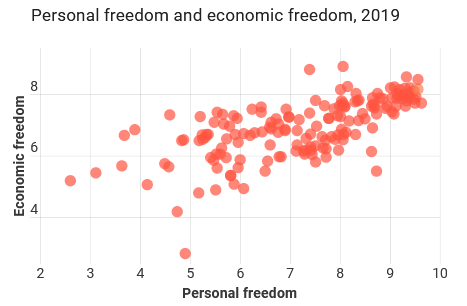

Personal and Economic Freedom

Personal and Economic Freedom

Source: Cato

Rules of the Economic Game

Reliable rules reduce risk and uncertainty.

The rules of the game include:

- laws protecting person and property are part of the rules of the game - laws enforcing contracts are part of the rules of the game - regulations are part of the rules of the game

- regulations can

promote competitive innovation (e.g., anti-trust)

or inhibit competitive inhibit (e.g., excessive patenting)

References

Coen, Corinne. (2009) Contrast or Assimilation: Choosing Camps in Simple or Realistic Modeling. Computational and Mathematical Organization Theory 15, 19--25. http://www.springerlink.com/content/mt3177867j468308/

Epstein, Joshua M. (2008) Why Model?. Journal of Artificial Societies and Social Simulation 11, Article 12. http://jasss.soc.surrey.ac.uk/11/4/12.html